Investing With Intention (Part 1)

How Lighthouse Planning Thinks About Building Portfolios

Most investment conversations start with whatever the market is doing right now.

That makes sense. The market is visible. It moves every day. There is always a headline, a chart, a forecast, or a smart-sounding person explaining what investors should be worried about next.

Interest rates. Elections. Inflation. AI. Recessions. Wars. Real estate. The Fed. The dollar. The next bubble. The last crash.

It never really ends.

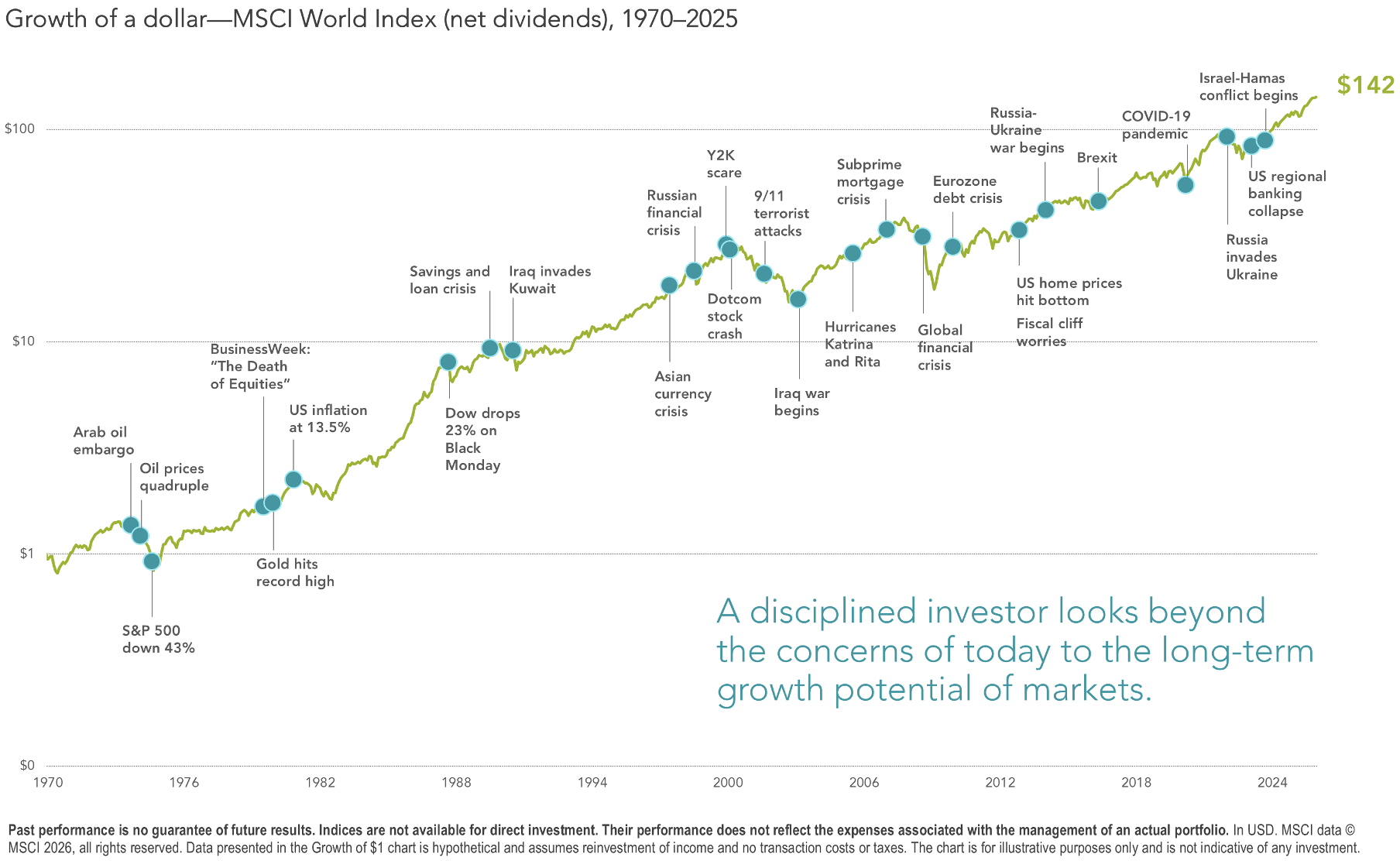

And while some of those things matter, they are usually not the best place to begin… nor are they helpful predictors for your investing success (see the chart below… the market has done well in the long run despite all the short-term chaos).

At Lighthouse Planning, we think the better starting point is more personal and more practical:

What does this money need to do for your life?

That question has a way of simplifying things.

Money you may need next year should not be invested the same way as money you hope to use 30 years from now. Money set aside for a home purchase should not carry the same risk as money meant to fund retirement. Money that helps your family sleep at night should probably not be chasing a slightly higher expected return if doing so puts an important goal at risk.

This is the foundation of our investment philosophy.

We do not react.

We do not predict.

We do not attempt to outguess the market.

Instead, we rely on academic and evidence-based investment strategies to stack the odds in your favor, providing a favorable long-term investment experience.

The Portfolio Serves the Plan

Look, as much as we prioritize life planning in our client engagements, portfolio management matters. Returns matter. The details are important.

But the portfolio is not the point.

The point is the life the portfolio is meant to support.

That may sound obvious, but it is easy to forget. The investment world has a way of pulling people into a conversation that feels more sophisticated than necessary. Performance comparisons, market outlooks, manager rankings, tactical moves, economic commentary. Most of this is just NOISE.

At Lighthouse Planning, we do not view investment management as something separate from financial life planning. The investment strategy should grow out of the plan.

That means we get clear about questions like:

When will you need this money?

How much risk does the plan actually require for you to reach your goals?

How much volatility can you live with emotionally?

What needs to stay liquid?

Where are the tax impacts?

What kind of flexibility would make you feel more confident?

What are you building toward?

Those questions may not sound as exciting as trying to predict the next market move, but they are far more useful.

A good portfolio should be technically sound. It should also be understandable. You should know what you own, why you own it, what it is designed to do, and what kind of behavior it will require from you when markets are uncomfortable.

Your portfolio isn’t some silo that you experience on its own.

You experience it while raising kids, running a business, buying a house, selling a company, changing careers, caring for parents, retiring, giving money away, or trying to figure out what kind of life you actually want next.

So the question is not,, “What is the optimal portfolio?”

The better question is, “What is the right portfolio for my ideal life?”

The Three-Bucket Framework

One of the ways we bring clarity to investment decisions is through a simple “Three-Bucket Framework”.

Don’t let it’s simplicity fool you – adhering to this framework will give you wisdom and resolve in your investing decisions that most don’t enjoy.

In my experience, most people do not need a more complicated investment philosophy. They need a clearer way to connect their money to their time.

At Lighthouse Planning, we generally organize money around three broad time horizons:

Short-Term Bucket: money needed within the next 0–2 years.

Mid-Term Bucket: money likely needed within 2–5 years.

Long-Term Bucket: money intended for 5+ years from now.

Each bucket has a different job. Once we know the job, we can be much more thoughtful about how the money should be invested.

Short-Term Bucket: 0–2 Years

For goals and needs coming up soon.

This might include an emergency fund, estimated tax payments, a home down payment, a business cash reserve, a planned renovation, a vehicle purchase, tuition, a sabbatical fund, or any other expense that is close enough that market volatility could create a real problem.

The job of this money is to be available (aka liquid and stable).

That usually means cash or cash-equivalent investments: checking, savings, CDs, money market funds, Treasury bills, or other short-term instruments when appropriate.

There is a trade-off here: You give up the possibility of higher expected returns in exchange for stability and access.

It can be tempting, especially for high earners and business owners, to look at cash and feel like it should be doing more. (And sometimes it should.. Too much cash held for too long can become a drag on a financial plan.)

But cash is not bad when given the right parameters (aka this bucket). .

Cash is what keeps you from selling long-term investments during a bad market. It lets you make a calm decision in a stressful season. It gives a business owner the courage to hire, invest, or take a slower month without spiraling. Sometimes it simply helps a family breathe.

That is not nothing.

Short-term money should not be forced to act like long-term money. It has a different job.

An example of how to determine what should sit in your short-term bucket for a “Sample Family”

$30,000 - Emergency Fund

$12,000 - Family Vacations

$10,000 - Half-Bath Renovation

$15,000 - Tax Payments

$4,000 - New Couch

$1,500 - Roadtrip with the kids

Total = $72,500 should be sitting in a high-yield savings account or similar

Mid-Term Bucket: 2–5 Years

Mid-term money requires more judgment.

This is money you do not need immediately, but also money that does not have enough time to recover from a major market decline.

It might be for a future home purchase, a business transition, the first few years of retirement spending, a meaningful family expense, or a goal where timing matters but is not necessarily immediate.

This money may be able to take some investment risk, but not as much as long-term money.

In many cases, this bucket, viewed on its own, would not be more aggressive than a balanced mix of stocks and bonds. Depending on the goal and the client’s flexibility, something around 50% stocks and 50% bonds (broadly diversified) may be the upper end of what we would consider for this time horizon.

The goal here is not to squeeze out maximum possible returns.

The goal is to pursue reasonable growth and/or income while respecting the fact that the money has a job to do relatively soon.

This is where high-quality fixed income can be useful. We often prioritize short-term, investment-grade bond ETFs in this part of the portfolio because they have (historically) helped provide more stability than stocks while still offering more return potential than cash over time.

Bonds are not risk-free! Interest rates move. Bond prices fluctuate. Credit quality matters. Duration matters.

When used thoughtfully, fixed income can help bridge the gap between cash and long-term growth assets.

This bucket should feel measured and tempered per your time horizon.

Long-Term Bucket: 5+ Years

Long-term money is built different (this is the exciting part!).

This is the money meant for retirement, future college funding, financial independence, legacy, or simply long-term wealth building.

Because the time horizon is longer, this money can stomach more volatility and risk. You have time to recover from a prolonged market downturn while your short-term and mid-term bucket fills the gap.

The stock market has never offered long-term growth without discomfort along the way.

There will be recessions. There will be bear markets.

There will be years where international stocks disappoint, small companies lag, value stocks look outdated, bonds feel frustrating, or cash suddenly feels emotionally safer than anything else.

This is a FEATURE, not a bug! It’s part of investing.

It does not mean we ignore risk and just gamble in the long-term bucket. It’s here that we respect and understand that short-term uncertainty is usually the price paid for long-term growth.

For this bucket, we generally prioritize globally diversified stock portfolios. We deploy an evidence-based approach to portfolio design. We prioritize ETFs from Dimensional Fund Advisors, creating risk-adjusted portfolios that consider your time horizons and your personal risk tolerance.

Without getting too into the weeds, a few of the reasons we use DFA’s funds to build client portfolios:

Low expense ratios (lower fees mean better returns for you)

Broad, global diversification

Efficient trading mechanics not tied to commercial benchmarks

Intentional tilt towards asset classes that have historically outperformed (small-cap, value stocks, and profitable stocks)

Commitment to the “science of investing” and long-term data

When investing in the stock market, there WILL be down periods. But historically, the up periods last longer and have a far greater magnitude.

This is the long-term bucket because it requires you to be patient enough to let the market work in your favor, achieving higher expected rates of return.

The word “expected” is important. Higher returns are not guaranteed. They are compensation for accepting uncertainty.

That compensation does not show up on a predictable schedule. It often shows up after periods when investing feels uncomfortable, boring, or even foolish.

This is why long-term investing requires more than a portfolio.

It requires a philosophy you can actually live with.

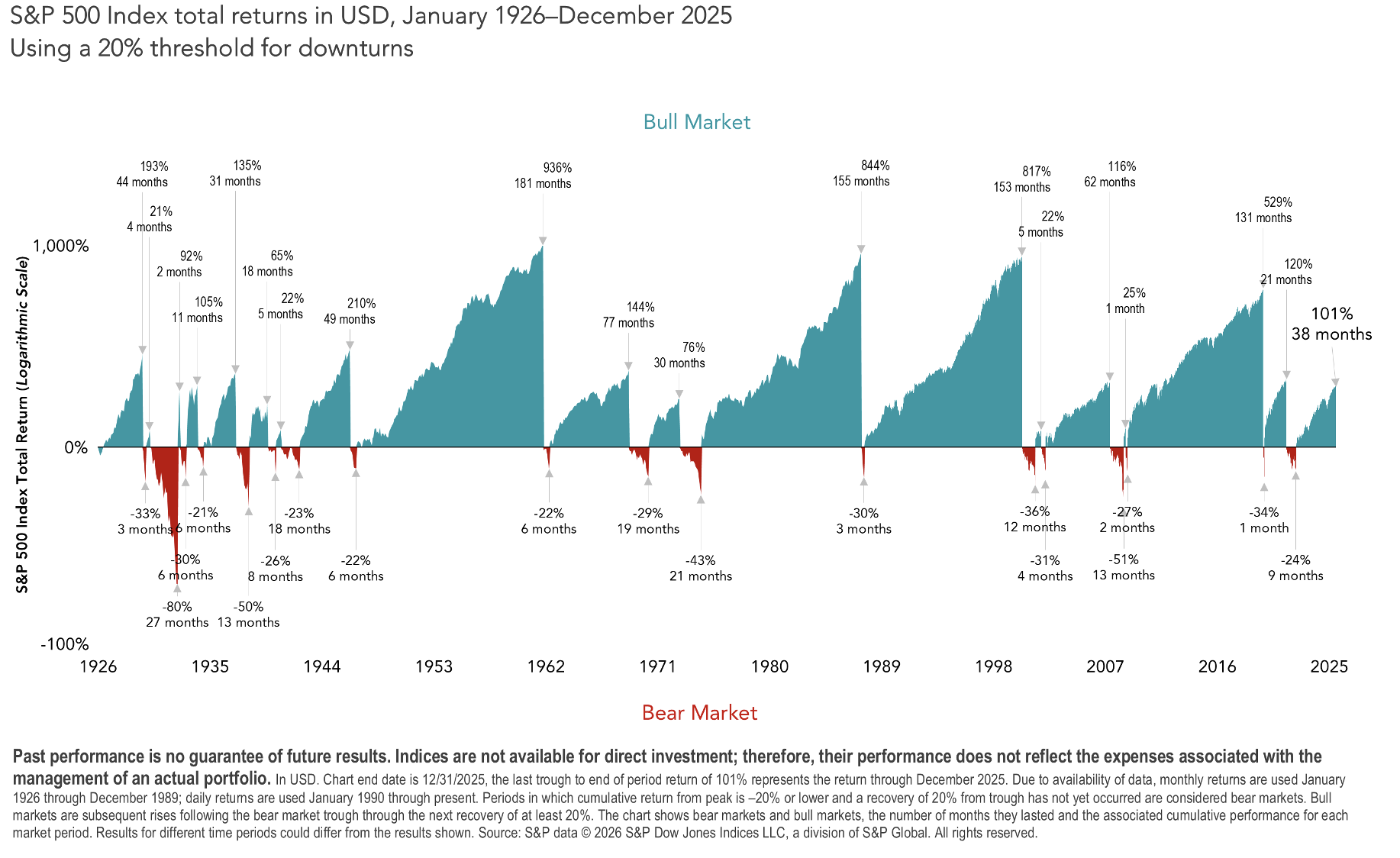

See the graph below for my favorite display of how much larger and longer bull markets are vs. bear markets historically.

Risk Is Not One Thing

People often talk about risk as if it has one definition. They are afraid of “stock market risk”, or “volatility”.

Risk is multifaceted and can come from many sources.

There is market risk, the risk that your investments decline in value as the whole stock market contracts.

But there is also liquidity risk, the risk that your wealth exists on paper but is not available when you need it. This happens if you have illiquid or highly volatile investments in your “short-term bucket”.

There is concentration risk, the risk of having too much of your net worth tied to one company, one business, one property, one industry, or one idea. This often happens with business owners and tech employees who have stock options.

There is tax risk, behavioral risk, inflation risk, and the very real risk of building a financial life that looks successful but feels misaligned (let’s grab a drink and I can share more about this last one!).

Part of our work is helping clients see these risks clearly so that they can take on the right risks on purpose.

For a young business owner with strong cash flow and decades ahead, the plan’s tolerance of risk may be greater. For a family preparing for a major home purchase or transition, we may “take some chips off the table” and derisk the portfolio per their time horizons. For a client whose wealth is concentrated in a business, real estate, or employer stock, diversification may matter more than chasing a slightly better return elsewhere.

The question is not, “Is this risky?”

The better question is, “Is this risk worth taking, given the rest of the plan?”

That is a more honest conversation.

We Do Not Build Around Predictions

I understand why people want market predictions.

Certainty is comforting. If someone could tell us what happens next, investing would feel much easier. But there would be no returns for your investment if things were certain.

The investment world has a long history of confident forecasts that did not age well.

To successfully time markets, you have to get several things right at once. You have to know what will happen, when it will happen, how much of it is already reflected in prices, how other investors will respond, when to get out, and when to get back in.

That is a hard way to build a financial life. We prefer to focus on what we can control.

How much risk are we taking?

Are we diversified?

Are costs reasonable?

Are we being tax-aware?

Does the portfolio match the time horizon?

Are we rebalancing thoughtfully?

Are we staying disciplined when the market feels uncomfortable?

Are we making changes because the client’s life changed, or because of something in the news?

That last question is REALLY important.

Virtually all portfolio changes should happen because something meaningful changed in your life, risk tolerance or timing…not because of short-term market movements or headlines.

A child was born. A business was sold. A house was purchased. A career changed. Retirement moved closer. Spending changed. A parent needed help. A new opportunity appeared. A goal became clearer.

Those are real reasons to revisit the plan.

The market will always give us something to react to. This is where discipline is the key. During volatile times, this refrain can be helpful… “don’t just do something, sit there!”.

I’ll continue to record my thinking/manifesto on designing investment portfolios for clients and share more soon. :)